Fixed Rate vs Adjustable Rate Mortgage: How to Choose

TL;DR: Fixed rate mortgages give you payment certainty for the life of the loan. Adjustable rate mortgages give you a lower starting rate in exchange for some future uncertainty. Neither one is always better. The right choice depends on how long you plan to stay in the home, what rates are doing, and how much variability you can comfortably handle. Call Peak Capital Mortgage LLC at (970) 577-9200 and we will model both options with your actual numbers.

In This Article:

The Core Difference in Plain English

How a Fixed Rate Mortgage Actually Works

How an Adjustable Rate Mortgage Actually Works

The Decision Framework: Four Questions to Ask Yourself

When Fixed Wins. When ARM Wins.

The One Thing Most People Get Wrong

The Bottom Line

The Core Difference in Plain English

When you get a mortgage, you are agreeing to pay back a large amount of money over time. The interest rate on that loan determines how much extra you pay on top of what you borrowed.

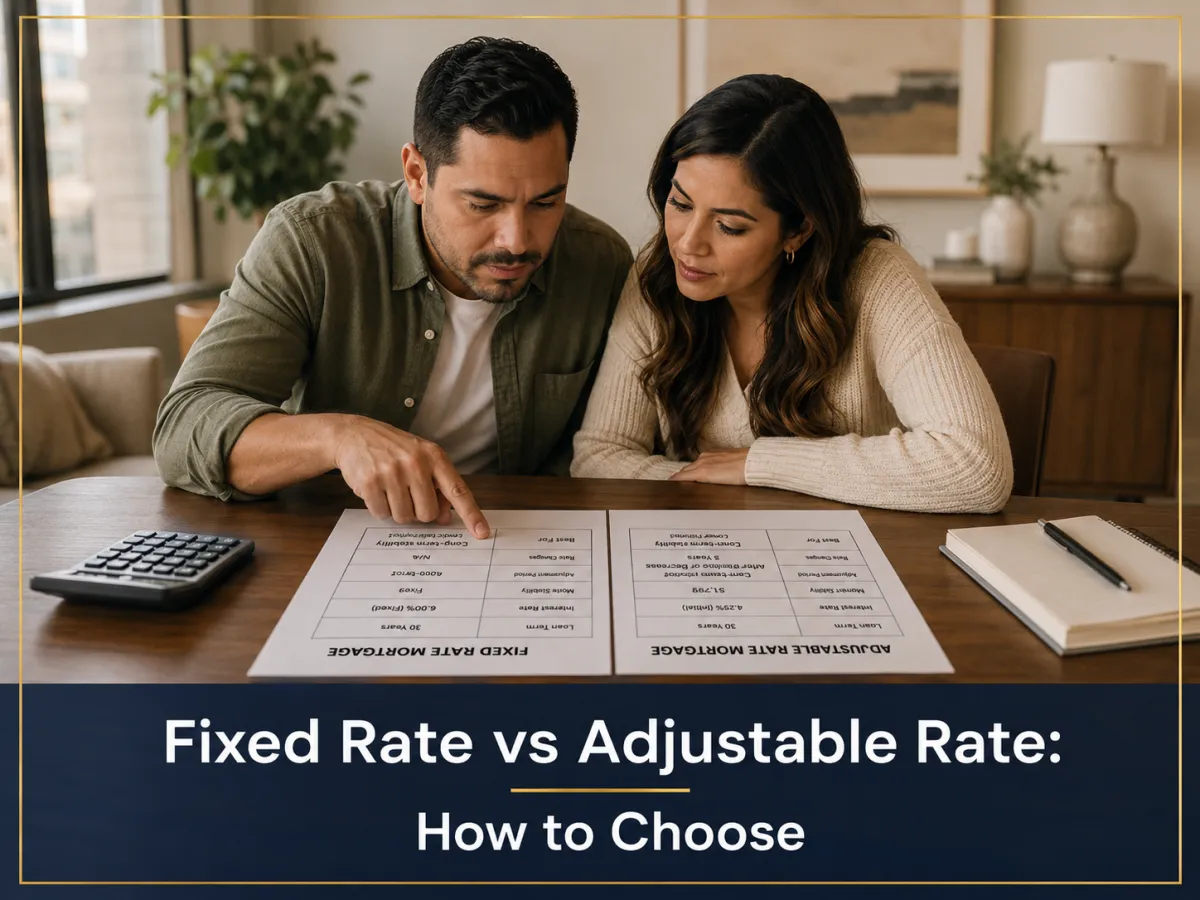

With a fixed rate mortgage, that rate is locked in for the entire loan term. It never moves. Your principal and interest payment on day one is the same as your payment in year 29.

With an adjustable rate mortgage, the rate is fixed for an initial period, typically 3, 5, 7, or 10 years, and then it adjusts periodically based on a market index. During the fixed period you have predictability. After that period ends, your rate and payment can go up or down based on where rates are at the time of each adjustment.

That is the whole thing. The question is which structure makes more sense for your specific situation.

How a Fixed Rate Mortgage Actually Works

The 30-year fixed mortgage is the most common home loan in the country for a reason. It is simple. You borrow money, you pay it back at a fixed rate over 30 years, and nothing about that arrangement changes regardless of what happens to interest rates in the broader economy.

The benefits are real. You can budget with confidence because your principal and interest payment never changes. If rates rise significantly after you close, you are insulated. You do not have to watch the market or worry about refinancing by a certain date.

The tradeoff is also real. Fixed rate loans typically carry a higher starting rate than comparable adjustable rate options. You are paying a premium for that certainty. Over a 30-year horizon that can mean a meaningful amount of additional interest paid, especially if rates stay flat or decline after you close.

One important clarification: your principal and interest payment stays fixed. If your loan includes an escrow account for property taxes and insurance, the total monthly amount you pay can shift over time as those costs change. The mortgage payment itself is locked. The escrow portion is not.

For full details on how the 30-year fixed works and whether it makes sense for your situation, visit our 30-year fixed mortgage page.

How an Adjustable Rate Mortgage Actually Works

An ARM starts with a fixed rate for an initial period. The most common structure today is the 5/1 ARM, which means your rate is locked for the first five years and then adjusts once per year after that. You can also find 7/1 and 10/1 structures depending on your lender and program.

After the fixed period ends, your rate adjusts based on a benchmark index, currently SOFR (Secured Overnight Financing Rate), plus a margin set at closing. If the index is higher when your rate adjusts, your rate goes up. If it is lower, your rate goes down.

The adjustment is not unlimited. ARMs have caps built into them. A typical structure includes an initial adjustment cap of 2%, a periodic cap of 2% per subsequent adjustment, and a lifetime cap of 5% over the starting rate. That means if you start at 6%, your rate can never exceed 11% over the life of the loan under that structure. That ceiling is real protection, though most borrowers using an ARM strategically should not expect to be in the loan long enough for it to matter.

The advantage during the fixed period is straightforward: the starting rate on an ARM is typically lower than a comparable fixed rate, often by half a percent to a percent and a half. On a large loan that difference in monthly payment is significant.

For more detail on ARM structures and who they work best for, visit our adjustable rate mortgage page.

The Decision Framework: Four Questions to Ask Yourself

This is where the decision actually gets made. Work through these four questions honestly and the right answer usually becomes clear.

Question 1: How long are you planning to stay in this home?

This is the most important question. If you are confident you will sell or refinance within five to seven years, an ARM's fixed period covers your entire ownership window. You get the lower rate for the full time you are in the home and you exit before any adjustment ever happens. The risk is essentially theoretical.

If you are buying your forever home, or close to it, a fixed rate removes the possibility of any unpleasant surprises. You pay a bit more for certainty, and over 20 or 30 years that certainty has real value.

Question 2: What does your monthly budget look like?

An ARM's lower starting payment can make a meaningful difference in what you qualify for and how much breathing room you have month to month. For some buyers, especially in high-cost markets or high-rate environments, the ARM's payment advantage is the difference between a comfortable budget and a tight one.

If you are already comfortable with the fixed rate payment, the lower ARM payment may be a nice-to-have rather than a necessity. That changes the risk calculus.

Question 3: Where are interest rates right now relative to history?

This one requires a bit of market awareness. When rates are historically high, ARMs make more strategic sense for buyers who believe rates will eventually come down. You take the lower ARM rate now, and when rates drop you either refinance into a fixed rate or your ARM adjusts downward. Either way you benefit.

When rates are historically low, fixed rates become more attractive. Locking in a low fixed rate for 30 years is a powerful position. The ARM's lower starting rate is less compelling when fixed rates are already favorable.

Question 4: How do you handle financial uncertainty?

This is honest self-assessment, not a trick question. Some people can look at an ARM's adjustment caps, understand the worst-case scenario, and be completely comfortable knowing they have a plan if rates move. Other people will lie awake at night wondering what their payment will be in year six.

Neither response is wrong. The mortgage that lets you sleep is often the right mortgage, even if the numbers slightly favor the other option.

When Fixed Wins. When ARM Wins.

Here is the honest breakdown.

Fixed rate tends to win when: You are buying a home you plan to stay in long term. Rates are currently low relative to historical averages and you want to lock that in. You want complete payment predictability without any market dependency. You have a budget that works comfortably at the fixed rate payment.

ARM tends to win when: You have a clear exit strategy within the fixed period, whether that is a planned sale, a relocation, or a known refinance window. Rates are elevated and you expect them to decline. You are buying a higher-priced home where the payment savings during the ARM's fixed period are substantial. You are financially flexible and can absorb a payment adjustment if your plans change.

The most common mistake is treating this as a permanent choice. An ARM is not a trap. You can refinance out of it into a fixed rate if circumstances change or if rates improve. Many borrowers plan for this from the start. If you are refinancing an existing mortgage and weighing your options there, it is also worth understanding how a cash-out refinance fits into the picture.

If you are financing a home above the conforming loan limit, there are additional factors worth understanding before you choose a loan structure. Here is a full breakdown of how jumbo loans work.

The One Thing Most People Get Wrong

Most people frame this decision as "which one is safer?" and default to fixed because it sounds more conservative.

The reality is that choosing a fixed rate when you are only going to be in the home for five years is not conservative. It is paying extra for protection you do not need. You are buying a 30-year insurance policy on a five-year situation.

Conversely, choosing an ARM on a home you plan to keep for 25 years and hoping things work out is also not a strategy. That is optimism without a plan.

The right framing is: which structure fits my actual timeline and situation? When you answer that honestly, the choice usually becomes straightforward.

The Bottom Line

Fixed rate mortgages and adjustable rate mortgages are both solid tools. The one that is right for you depends entirely on your timeline, your budget, your risk tolerance, and where the rate environment sits when you are buying.

At Peak Capital Mortgage LLC we model both scenarios side by side for every client. You see the actual payment difference, the total interest comparison over your expected ownership window, and the realistic risk picture for the ARM option. Then you make the call with full information.

We are independent, which means we work for you and not for any single lender. We have access to multiple programs and rate options across both fixed and adjustable structures.

Call us at (970) 577-9200 or schedule a consultation to get started.